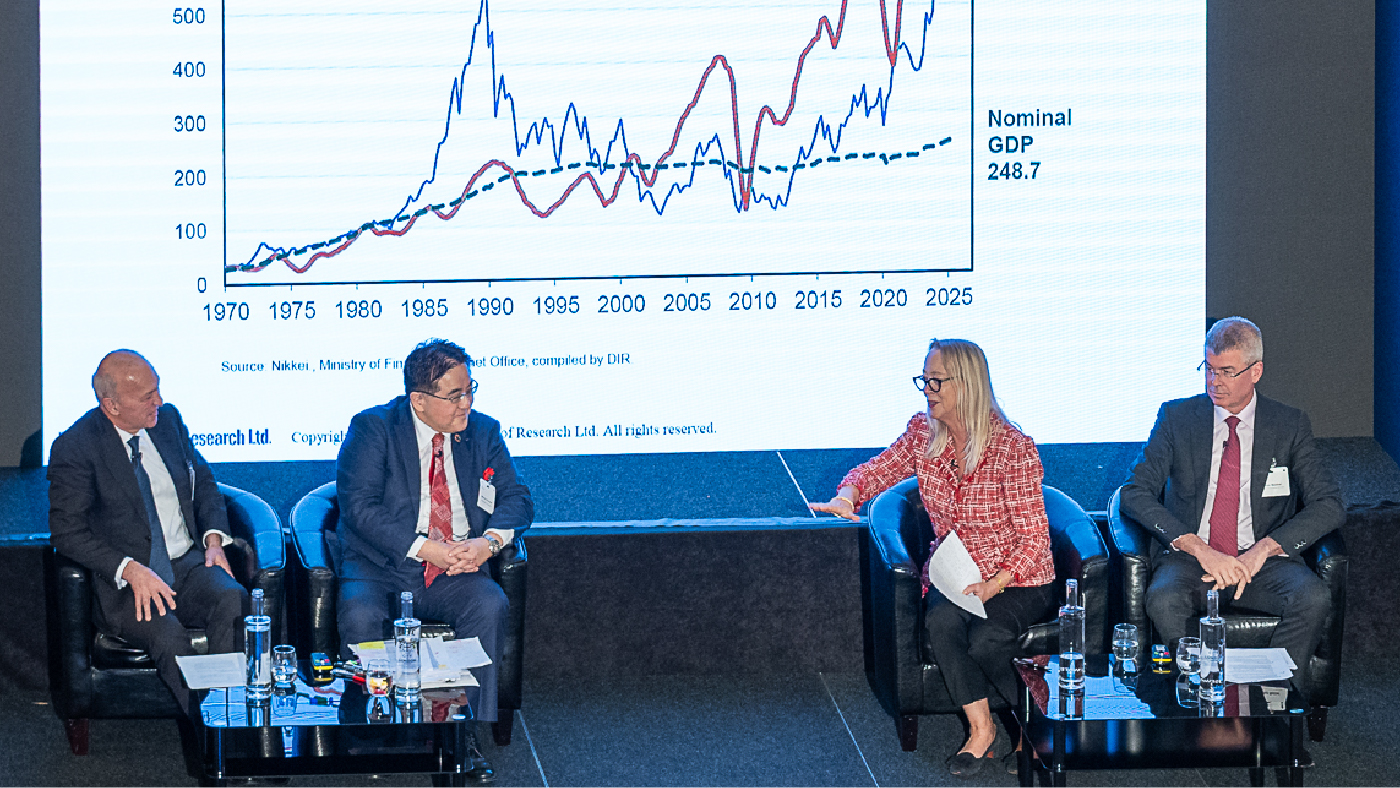

This panel examined three things: the current situation of the Japanese economy, risks and, finally, opportunities.

For Kumagai, the Japanese economy is at a historical turning point. Structural changes are accelerating as the economy emerges from deflation, wage hikes gather momentum and capital investment increases. Supporting factors include improvements in the household income environment, government economic policy and continuing accommodative monetary policy. Kumagai sees Japanese stocks as undervalued relative to corporate profits.

Although mindful of the highly cyclical nature of the Japanese economy, Webber described Japan as an “incredibly vibrant and exciting market” with key technologies and some very good companies, providing a way to diversify away from U.S. equities. Particularly positive developments were the material increase in the number of companies buying back shares and the decline in companies trading at below book value.

What about downside risks? Kumagai reeled off five: The Trump tariffs; the deteriorating Japan-China relationship; escalating tensions in the Middle East and Ukraine; a sharp drop in the yen exchange rate; and rising domestic interest rates. For now, Prime Minister Takaichi is maintaining fiscal discipline, but that could change. “In the future, the administration’s expansionary fiscal policy might carry the risk of a yen depreciation cycle and a rise in long-term interest rates,” Kumagai commented.

Webber was worried about Japanese companies’ possible complacency in the face of the competitive threat from China, “an emerging giant and incredibly strategic in its investment, whether electric vehicles, the battery supply chain, or healthcare and pharmaceuticals.” On the market side, vulnerabilities he highlighted were the steepening of the yield curve, volatility in JGBs and the risk of rapid yen strengthening.

As the author of the influential book The 100-Year Life, Gratton’s focus was on demography. As Japan’s population ages and shrinks, the traditional three-stage life of full-time education, full-time work and full-time retirement is breaking down and needs to be replaced by the multi-stage life, with lifelong education, greater flexibility at work and a later retirement age. While Japan is doing exceptionally well on the healthy aging front, some Japanese organizations are proving too hierarchical and bureaucratic to embrace more flexible and amenable working conditions. Immigration, meanwhile, is needed to fill the skills gap. Is there any viable solution to population decline itself? Gratton pointed out that while some governments have managed to restrict the number of children women can have, none have ever succeeded in getting them to have more.

What, finally, about opportunities? If Japan can increase three key factors — labor input, capital stock and total factor productivity (TFP) — Kumagai believes that it could achieve a high-growth scenario, with annual economic growth of 1.5% through to 2040. For his part, Webber saw an opportunity in Japan’s best businesses ditching the bad habit of hoarding cash and achieving better capital efficiency. He also noted that the conventional view that a weak currency is good for Japanese stocks is out of date and that the combination of a strong stock market with a strong yen would be a major plus for foreign investors. The positives that Gratton singled out included soft power and social cohesion. “When you see what the lack of social cohesion does to a society, does to its economy, you realize this is a very important intangible asset,” she said.